Regret Bounds for Risk-sensitive Reinforcement Learning with Lipschitz Dynamic Risk Measures

{kind=link}

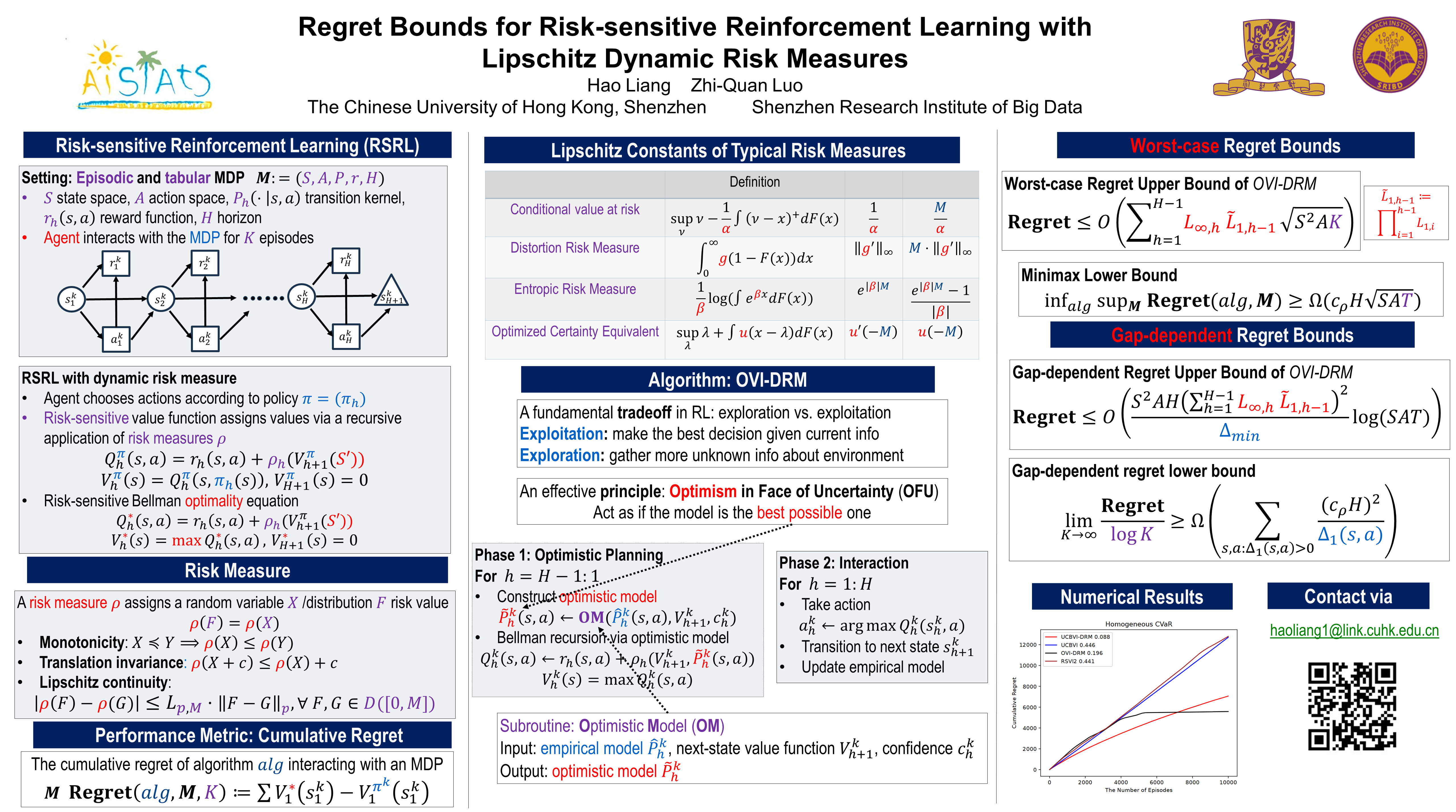

Abstract

We study finite episodic Markov decision processes incorporating dynamic risk measures to capture risk sensitivity. To this end, we present two model-based algorithms applied to \emph{Lipschitz} dynamic risk measures, a wide range of risk measures that subsumes spectral risk measure, optimized certainty equivalent, and distortion risk measures, among others. We establish both regret upper bounds and lower bounds. Notably, our upper bounds demonstrate optimal dependencies on the number of actions and episodes while reflecting the inherent trade-off between risk sensitivity and sample complexity. Our approach offers a unified framework that not only encompasses multiple existing formulations in the literature but also broadens the application spectrum.