Testing exchangeability by pairwise betting

Aytijhya Saha ⋅ Aaditya Ramdas

2024 Poster

{kind=link}

Abstract

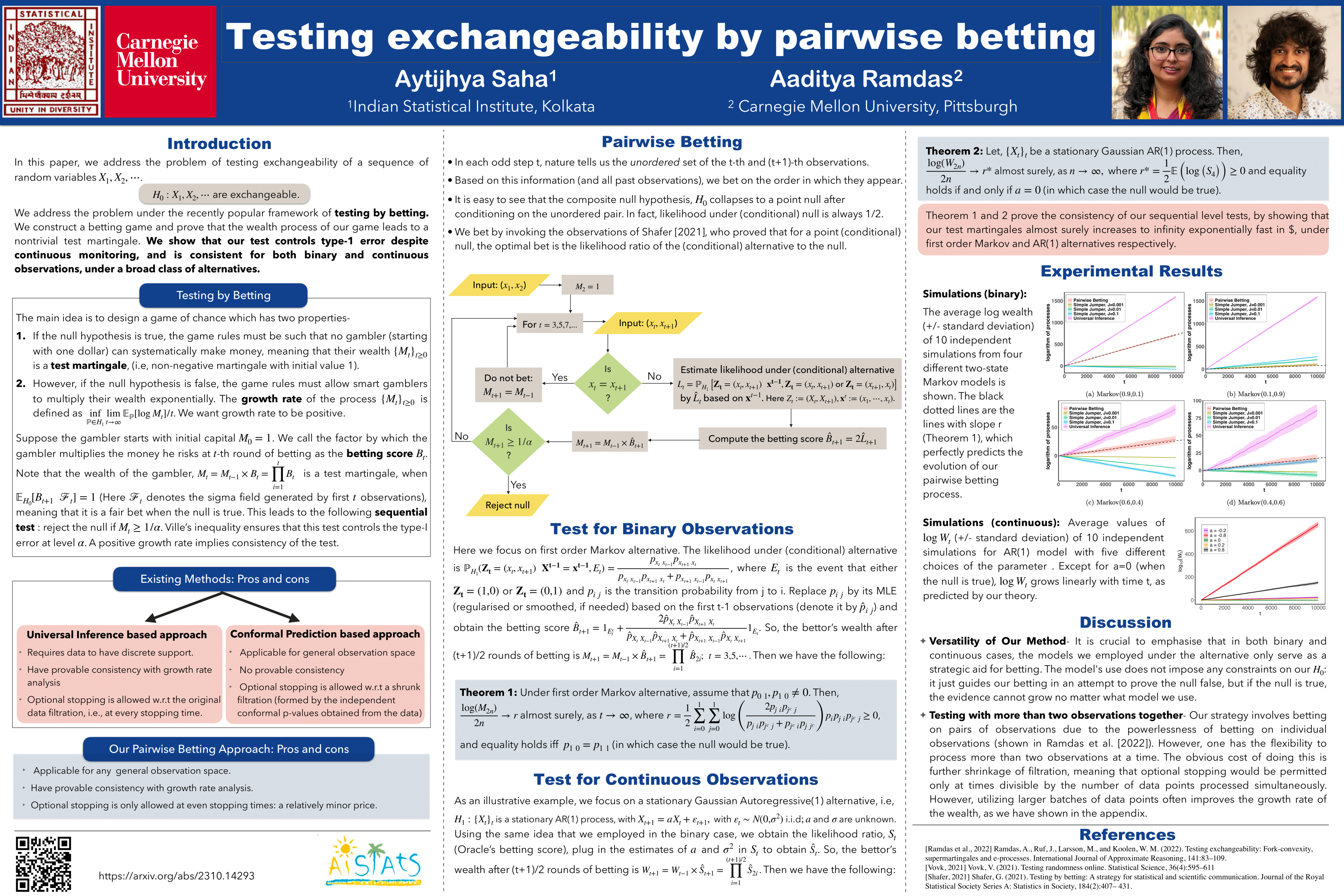

In this paper, we address the problem of testing exchangeability of a sequence of random variables, $X_1, X_2,\cdots$. This problem has been studied under the recently popular framework of \emph{testing by betting}. But the mapping of testing problems to game is not one to one: many games can be designed for the same test. Past work established that it is futile to play single game betting on every observation: test martingales in the data filtration are powerless. Two avenues have been explored to circumvent this impossibility: betting in a reduced filtration (wealth is a test martingale in a coarsened filtration), or playing many games in parallel (wealth is an e-process in the data filtration). The former has proved to be difficult to theoretically analyze, while the latter only works for binary or discrete observation spaces. Here, we introduce a different approach that circumvents both drawbacks. We design a new (yet simple) game in which we observe the data sequence in pairs. Even though betting on individual observations is futile, we show that betting on pairs of observations is not. To elaborate, we prove that our game leads to a nontrivial test martingale, which is interesting because it has been obtained by shrinking the filtration very slightly. We show that our test controls type-1 error despite continuous monitoring, and is consistent for both binary and continuous observations, under a broad class of alternatives. Due to the shrunk filtration, optional stopping is only allowed at even stopping times: a relatively minor price. We provide a variety of simulations that align with our theoretical findings.

Chat is not available.

Successful Page Load