Smoothness-Adaptive Dynamic Pricing with Nonparametric Demand Learning

Zeqi Ye ⋅ Hansheng Jiang

2024 Poster

{kind=link}

Abstract

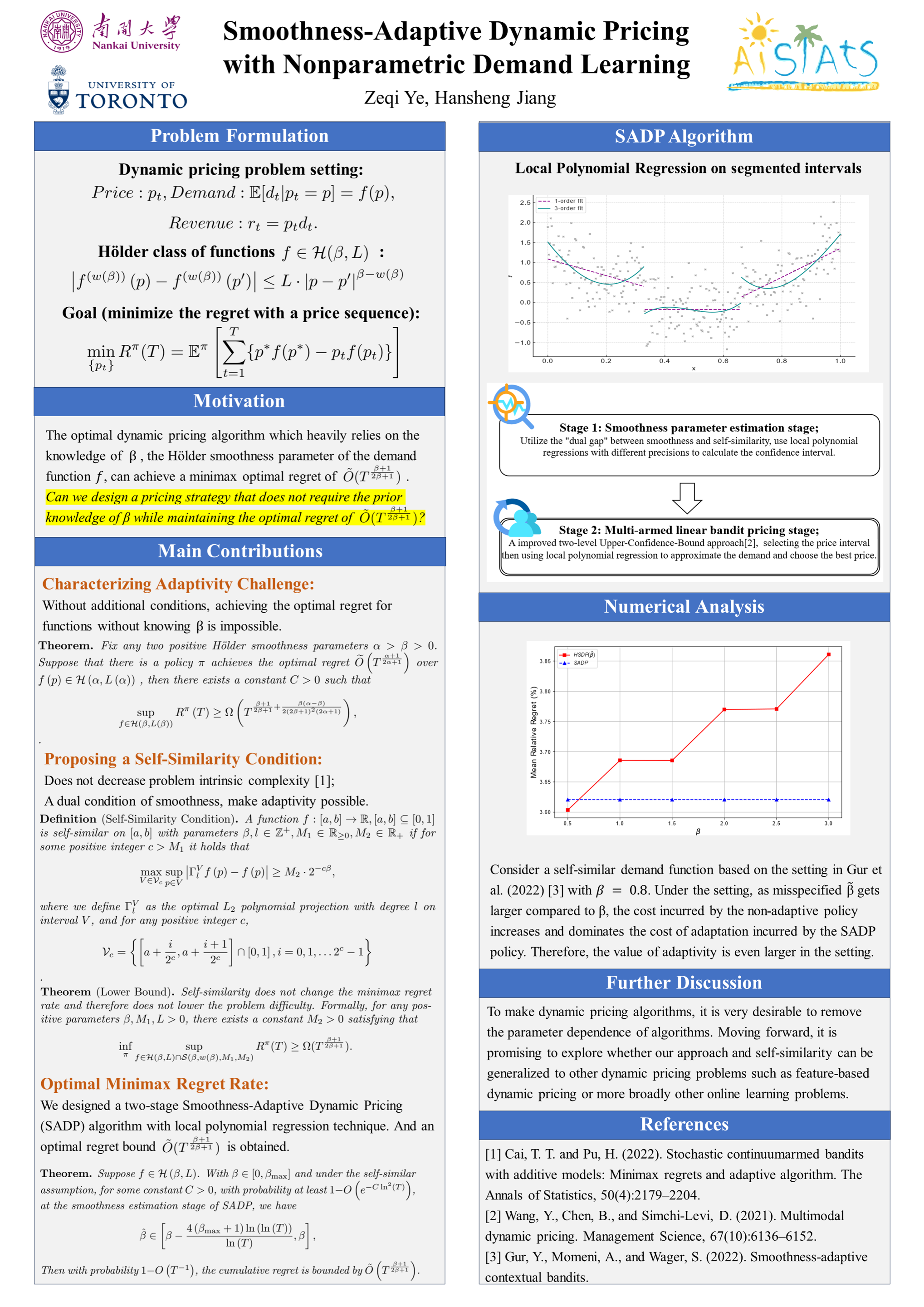

We study the dynamic pricing problem where the demand function is nonparametric and H\"older smooth, and we focus on adaptivity to the unknown H\"older smoothness parameter $\beta$ of the demand function. Traditionally the optimal dynamic pricing algorithm heavily relies on the knowledge of $\beta$ to achieve a minimax optimal regret of $\widetilde{O}(T^{\frac{\beta+1}{2\beta+1}})$. However, we highlight the challenge of adaptivity in this dynamic pricing problem by proving that no pricing policy can adaptively achieve this minimax optimal regret without knowledge of $\beta$. Motivated by the impossibility result, we propose a self-similarity condition to enable adaptivity. Importantly, we show that the self-similarity condition does not compromise the problem's inherent complexity since it preserves the regret lower bound $\Omega(T^{\frac{\beta+1}{2\beta+1}})$. Furthermore, we develop a smoothness-adaptive dynamic pricing algorithm and theoretically prove that the algorithm achieves this minimax optimal regret bound without the prior knowledge $\beta$.

Chat is not available.

Successful Page Load